Submitted by QTR's Fringe Finance

As I first noted back in 2023, my disdain, distrust and general disgust for financial media reached a peak in 2016 when CNBC’s Fast Money invited Bill Fleckenstein on the air to offer up his take on the economy and why the Fed-fueled market was “un-shortable”.

Bill is a well-known advocate for the Austrian school of economics and has been highly critical of the Fed and central banking policies for decades.

In this interview, he made two key points: 1) he thought Japan would probably be the first bond market to blow up and 2) he was buying gold and miners and thought the broader market was “un-shortable”. Fleckenstein told the hosts:

“Probably the first bond market to crack up will be in Japan but maybe it won’t. Maybe it’ll be here. I don’t really care if I miss the first break because they’re gonna come with QE4. The trade I want to catch is when people wake up to the fact that these Central Bank strategies are failures. They are the arsonists that create the fire, they’re not the firemen that put it out, even though they claim to be the latter.”

Seymour responded:

“But Bill, it sounds like you missed a lot. I mean, you’ve been on the show a number of times where you’ve been licking your chops and saying it’s about to happen, and it’s two, three years going on doing this, and a lot of this sounds kind of pathetic.”

Fleckenstein responded that’s he’s long gold and miners, prompting Seymour to take sarcastic shots at him, stating:

“Is gold going to $2,000 an ounce? Is it? I bet you bought gold at the bottom.”

To which Fleckenstein, rightfully pissed off, responds:

“I happened to catch the lows, but that does not mean anything. I’m not here to brag. I don’t ask to come on this show — you guys ask me. So don’t get in my face because I’m not joining the party you want me to.”

You can watch the full interview free here.

As I wrote back in 2023, "timing these assholes is everything” and today, here we are, about 9 years since that interview on an evening where it looks damn close to exactly what Bill Fleckenstein was ridiculed for on national television is happening. Japanese bonds are in a “full blown melt-down”, as Zero Hedge described it tonight:

It’s a move that Peter Schiff predicts “could force the Japanese government to sell Treasuries to service its debt.”

“It’s the Takaichi trade in motion. The combination of rising JGB yields in Japan and concerns over renewed US-European tariffs could lead to further rises in global bond yields, ” Mansoor Mohi-Uddin, chief macro strategist at Bank of Singapore told Bloomberg overnight.

Other strategists like Tadashi Matsukawa, head of bond investments at PineBridge Investments Japan are predicting MOF bond buying: “With interest rates rising this much, calls for the BOJ to conduct emergency operations and the Ministry of Finance to implement buybacks are likely to intensify.”

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

And while the Japanese bond market is imploding, gold is exploding even further to the upside, as it has been doing basically non-stop since dickhead Tim Seymour decided to make a snide comment about it in 2016.

Gold spot broke over $4,700/oz. tonight, extending what can only be described as a biblical move higher since the Seymour 10 Year Bottom™.

In the same vein, CNBC staple Josh Brown made a post in 2019 stating that “Permabears Are Ridiculous People” for celebrating small drawdowns in an otherwise rising nominal price stock market. I agree with Brown’s point on markets, but not that permabears are ridiculous — in fact, I find them to be the only people who see the market clearly.

And while both the Japanese bond and gold markets continue to make Tim Seymour look like even more of a turbo-douche than he made himself look back in 2016, gold has also humilated the above “yeah but the market hasn’t crashed, bro” argument that many perma-bulls use to try and disarm perma-bears (read: skeptics with common sense).

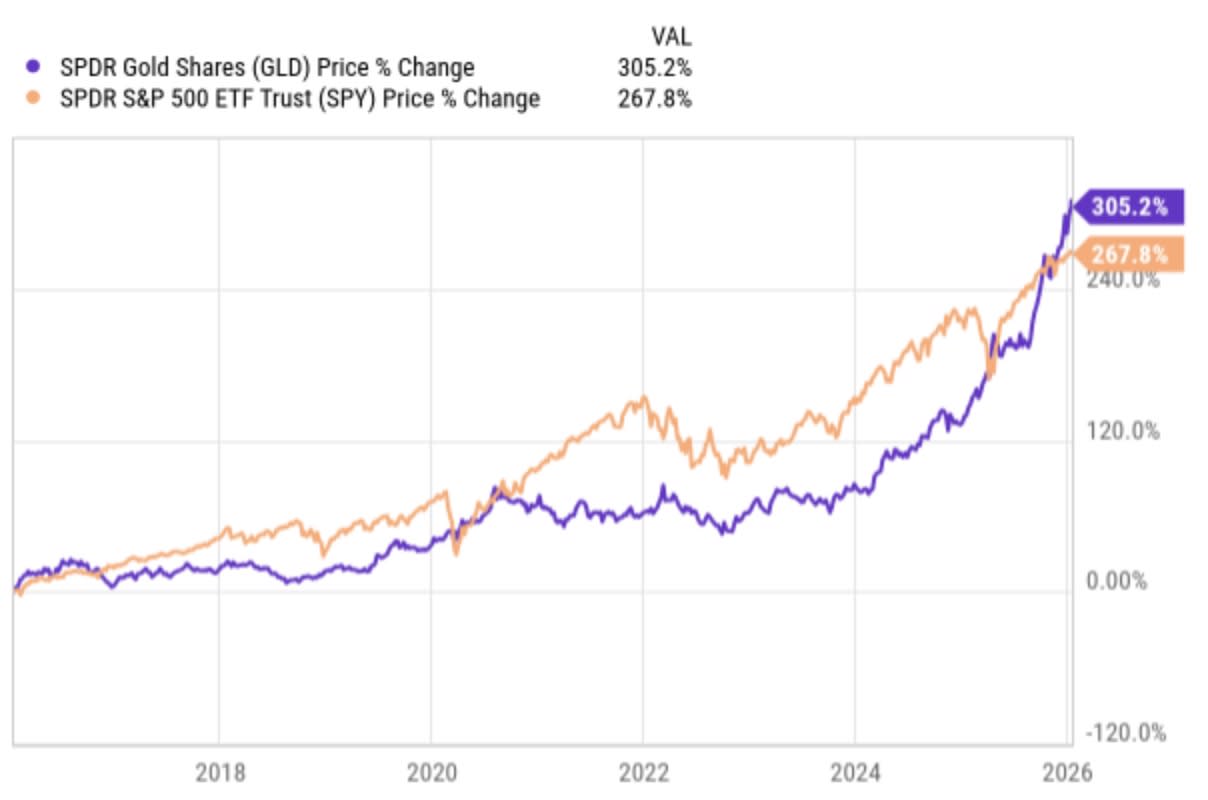

Because since Seymour’s shit fit, the price of gold has also beaten the holiest of holies, the S&P 500 average, rising about 300% versus the S&P’s 267% over the last 10 years.

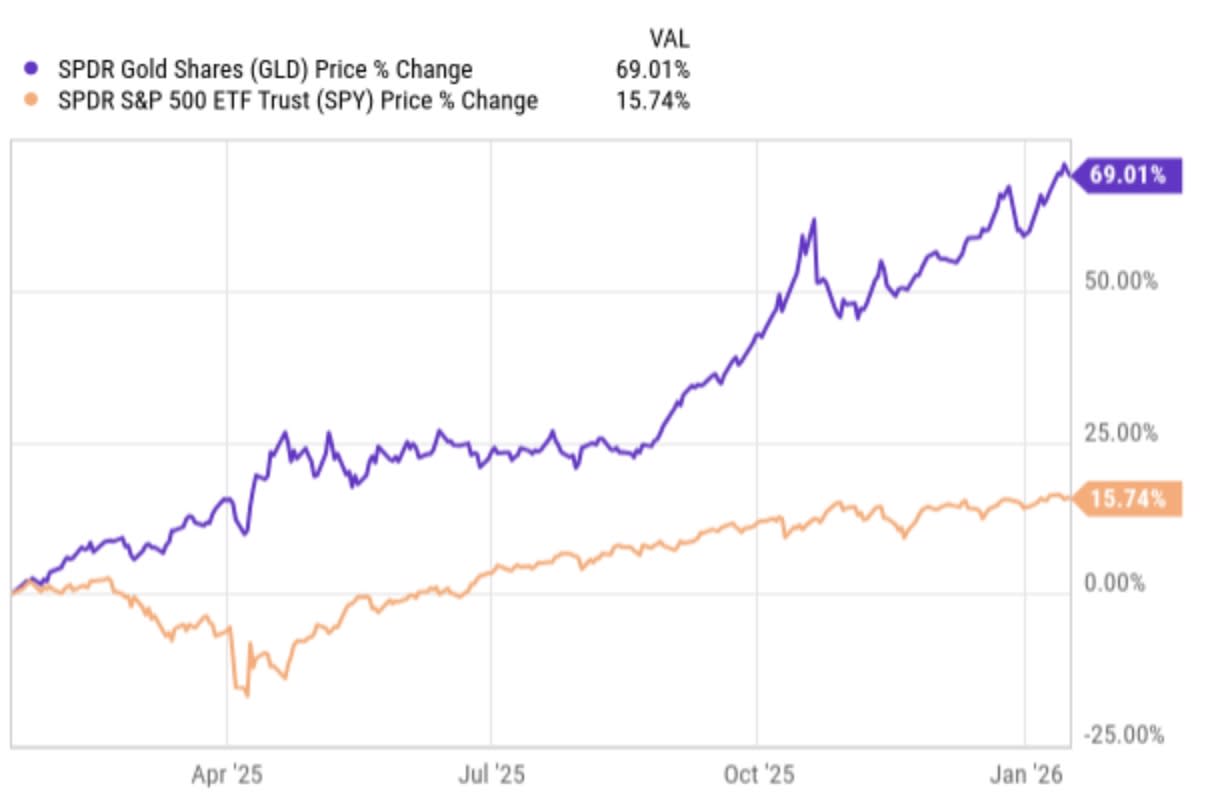

And in the last year, the contrast is even more stark and the trade has accelerated, with gold beating the S&P by about 54%.

So what did we learn? That being early is indistinguishable from being wrong if your referee is a CNBC talking head whose entire job depends on never admitting structural failure. Financial media doesn’t analyze risk: it mocks it, belittles it, and shames it until it goes away or blows up. And when it finally blows up, they pretend it was unforeseeable and complex instead of the obvious consequence of policies they cheered for a decade straight.

Tim Seymour didn’t just miss the trade — he missed the point. The point was never timing the top tick or calling the crash date like a carnival psychic. The point was recognizing that a system built on permanent intervention, debt monetization, and asset inflation eventually eats itself.

Gold wasn’t a “pathetic” trade; it was an insurance policy against institutional dishonesty. Japanese bonds weren’t a fringe worry; they were the logical pressure point in a world where yield suppression became national policy. Bill Fleckenstein didn’t “miss a lot” — he refused to play musical chairs with a blindfold on.

And that’s why this matters. Because the people who were mocked, sidelined, and shouted down weren’t permabears — they were adults. They understood cycles, incentives, and consequences in a market that hasn’t allowed consequences for far too long. Today, as Japanese bonds convulse and gold rips faces off, the only thing more inflated than asset prices over the last decade was the confidence of the people paid to sneer at those warning you it couldn’t last forever.

The Seymour interview is what inspired me to start a podcast and, eventually, a Substack. I knew then Bill was on to something that mainstream financial newsmedia would never understand. Today, the price of the market, gold and Japanese bond yields confirm both Bill and I were dead on balls accurate.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.